Recognition of Revenue From Sale of Finished Goods Is:

Is a product cost. A claims exchange transaction.

Mgt220 Chapter 6 Revenue Recognition Team Study

The revenue recognition concept is part of accrual accounting meaning that when you create an invoice for your customer for goods or services the amount of that invoice is recorded as revenue at.

. The main condition for recognising revenue is that. For the same reason we have Sales of Goods Act. Î the sale of goods.

As transfer to b which becomes a raw material for b. However in terms of IFRS for SMEs a sales transaction may only be recorded as revenue for accounting purposes when certain requirements are met and at a value determined according to the guidelines as set out in IFRS for SMEs. Although the timing of transfer under the two models will often coincide this different approach.

The revenue recognition principle of ASC 606 requires that revenue is recognized when the delivery of promised goods or services matches the amount expected by the company in exchange for the. Recognition of revenue from sale of finished goods is. This is where revenue recognition comes into play.

Thus the company cannot recognize the revenue on the 100 units sold for 200000 ie 2000 sales price per unit at the time of sale and should wait until the return period expires. The company issued a three-month return policy to its distributors. The receipt of interest royalties or dividends arising from the use of entity assets.

It is generally accepted that sales transactions of goods result in revenue at the time the transaction takes place. Completed Contract Method CCM. Construction contracts in which the entity is the contractor.

AS 9 Revenue Recognition is concerned with the recognition of revenue arising in the course of ordinary activities of the enterprise from. The company High Turnover Ltd. After youve finished configuring the settings for the released product you must manually define the revenue price by entering the fair value price or the median price if youre using median price method on the Revenue prices page go to Revenue recognition Setup Inventory setup Released products and then on the Action Pane on the.

Under standard costing companies typically record inventory including WIP at cost and then recognize revenue once they sell the product. Bs finished product are sold to outsiders as well as sold to c division. For job costing revenue recognition typically happens based on the percentage-of-completion or completed-contract method.

Although the timing of transfer under the two models will often coincide this different approach may result. In order to understand whether we can recognize revenue in respect of such goods which have been sent under sale or return option we have to understand the basic recognition principle or criteria given by International Accounting Standard IAS 18 Revenue. Recognition of revenue from sale of finished goods is.

View the full answer. O An asset source transaction. Revenue can ultimately be dubbed the heartbeat of the entity.

An asset source transaction. Revenue Recognition Practices. Select the incorrect statement regarding the recognition of depreciation on manufacturing equipment.

The revenue recognition guidance under FRS 102 allows accountants to determine at which point a sale can be recorded in a companys accounts as revenue. Multiple Choice An asset use transaction. REVENUE RECOGNITION RECAP WITH SPECIFIC FOCUS ON THE SALE OF GOODS.

Finished goods and therefore is in the scope of ASC 606. Until then the amount of cash received should be recognized as a liability entitled such as deposits received from. An asset exchange transaction.

Under IAS 18 the timing of revenue recognition from the sale of goods is based primarily on the transfer of risks and rewards. The associated cost of goods sold for the 100 units was 120000 ie 1200 cost per unit. Revenue can generally be categorised into four categories.

Revenue is recognized at a point in time when the control passes to the customer. Did you know that entities should not presume that revenue should be recognized at a point in time for the sale of goods under the FASBs new revenue standard the guidance in ASU 2014-091 as amended2. IFRS 15 instead focuses on when control of those goods has transferred to the customer.

Sorting through the details. - Sales of products. At Which Point can Revenue be Recognised for the Sale of Goods Under FRS 102.

Under IAS 18 the timing of revenue recognition from the sale of goods is based primarily on the transfer of risks and rewards. IFRS 15 instead focuses on when control of those goods has transferred to the customer. As of date of sale or delivery to customers.

Bill-and-hold basis recognizes revenue at the point of sale with goods delivered at a later date. However if the entity gives up raw materials or work in process for a finished good eg crude oil exchanged for gasoline the exchange generally would be considered a transaction to facilitate sales to customers and would be recognized at the carrying amount of the inventory. Is an overhead cost.

The Sales under CIP or CIF terms requires the Company to be responsible for providing freightshipping services as principal after the date that the Company transfers control of the metal in concentrate to its customers. Definition of Revenue Recognition. Revenue recognition principle states that revenue is recognized when it is realized received in cash or realizable will be received in cash and earned the firm has performed its part of the deal.

That is under the ASU revenue from the sale of what many would consider goods eg customized products may be recognized over. Coming back to the question. Common sources of revenue and point at which recognition occurs.

Provided that the other criteria for revenue recognition are met the staff believes that Company R should recognize revenue from sales made under its layaway program upon delivery of the merchandise to the customer. The accounting principle regarding revenue recognition states that revenues are recognized when they are earned transfer of value between buyer and seller has occurred and realized or realizable collection is reasonably assured.

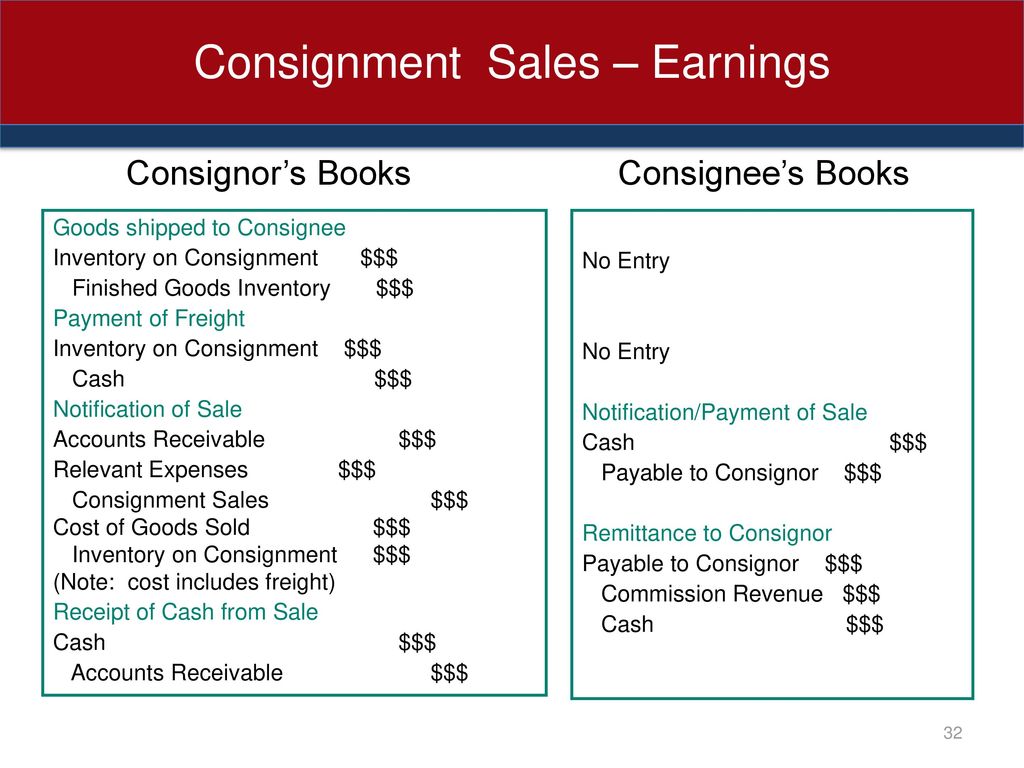

Ch 05 Part A Revenue Recognition Ppt Download

Chapter 6 Revenue Recognition Ppt Download

C H A P T E R 18 Revenue Recognition Ppt Download

Comments

Post a Comment